South Africa sending positive signals to global commerce

South Africa is not the easiest place to operate. We have seen high unemployment, years of debilitating load shedding, a greylisted financial system, and a sovereign credit rating that hadn’t moved in nearly two decades. South Africa provided global merchants plenty of reasons to look elsewhere.

That is shifting. Not because the structural challenges have vanished. Rather, a combination of meaningful signals - in payments infrastructure, financial crime compliance, cross-border settlement, and crypto regulation - have converged into a compelling case for reconsideration.

We work with global merchants making real decisions about where to expand.

Here’s what has changed in South Africa recently, and why it matters…

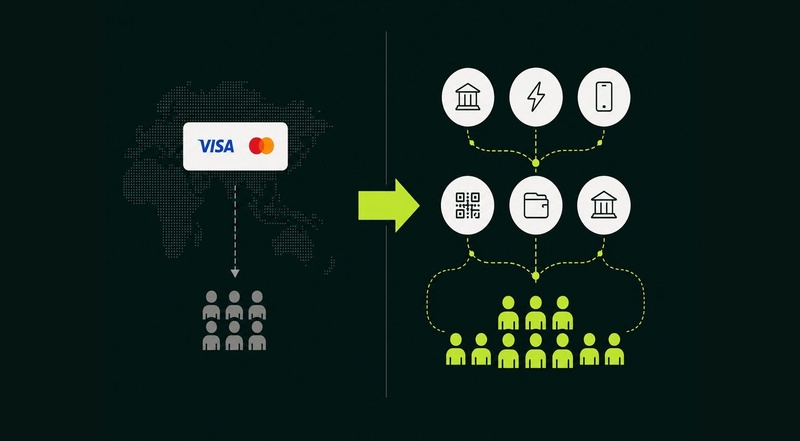

The South African Reserve Bank is modernising payments:

Historically, South Africa has faced systemic challenges from cash dependence to legacy clearing and settlement systems. The SARB’s Payments Ecosystem Modernisation (PEM) Programme has created buzz across local Fintechs of late. PEM presents definitive strides by the Reserve Bank to establish the framework for modernised payment infrastructure.

It’s an ambitious plan with intentions for real-time digital payments to be a genuine cash alternative and promote greater interoperability through National Payments Utility. (NPU). NPU essentially offers core payments infrastructure used for money movement, transaction clearing and enhanced interoperability across the financial ecosystem. Relevant global comparisons are UPI in India and Pix in Brazil offering shared infrastructure, real-time payments and fintech participation. The proof of concept is obvious in our view. There are also a host of other initiatives including eKYC for faster onboarding and fraud intelligence offering sophisticated compliance. These upgrades mirror what we're seeing across leading fintech, payments and global commerce. For global merchants, it offers reduced merchant friction, faster onboarding and more efficient settlement when entering South Africa.

South Africa’s removal from the FATF grey list

The Financial Action Task Force (FATF) sets global standards around anti-money laundering (AML) and financial crime controls. South Africa was added to the grey list in February 2023 for ‘increased monitoring’. The recent delisting is a major positive marker. It reflects progress in regulatory standards.

Naturally, this shift strengthens confidence in South Africa as a place to invest, trade and do business as it reduces friction associated with correspondent banking, onboarding, cross-border settlements and even investor diligence. For global merchants assessing new markets, these headlines matter. It means the local economy is aligned with global compliance standards.

"South Africa's progress in addressing the AML/CFT deficiencies and exiting the FATF greylist represents a major policy and institutional achievement for the people of South Africa."

— National Treasury, Republic of South Africa, 24 October 2025

The FATF delisting has not stood alone. Adding further weight to this momentum, Moody's upgraded South Africa's sovereign credit rating outlook to 'positive' this month. The first such improvement since 2007 highlighting an uptick in international confidence in the country's fiscal trajectory and reform commitments.

South African banks join China's Cross-Border Interbank Payment System

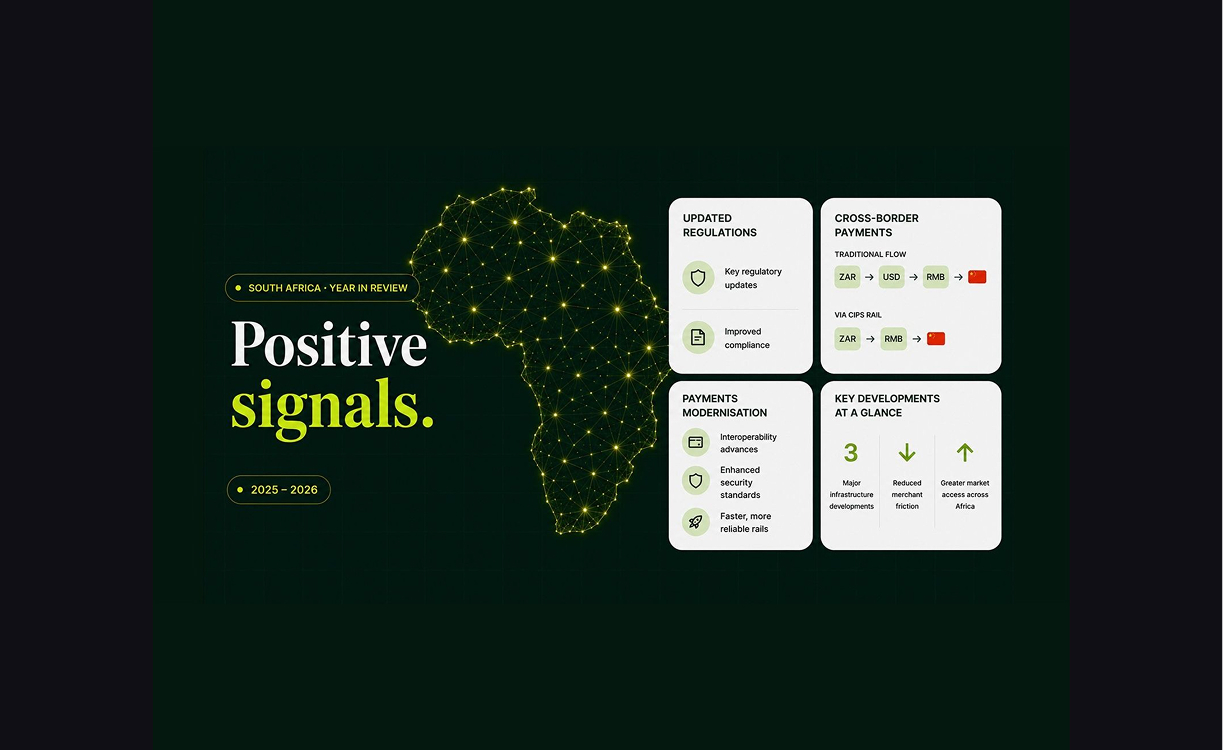

South Africa's payment rail connectivity is accelerating - Standard Bank led the way on CIPS, and ABSA has since followed. CIPS is China’s cross-border payment and settlement network, launched in 2015 and backed by the People’s Bank of China. It complements SWIFT while enabling more direct RMB* settlement.

For businesses moving money between Africa and China, faster clearing, fewer intermediaries and lower FX friction is unlocked. This is due to the reduced reliance on other major global currencies (like USD or Euro) in the flow of funds. With trade links across manufacturing, retail, construction, and imports continuing to grow, this infrastructure is well-positioned to optimize capital flows and improve settlement rails.

To illustrate, a traditional flow of funds for a South African business to pay a Chinese supplier would be:

ZAR → USD → RMB → China

This new rail through CIPS means that same South African business can pay the supplier in China:

ZAR → RMB → China

*RMB, short for Renminbi, is the currency of China where the unit of measurement is the (CNY) or the Chinese yuan which is commonly known.

What It means for merchants

For global merchants, market readiness is never just about demand. We believe the better question is infrastructure: How quickly can you launch? How easily can you accept local payments? How efficiently can you move money across borders?

South Africa is answering those questions more convincingly than it could a few years back. Less friction in payment infrastructure, stronger settlement rails, clearer compliance posture.That's the environment Novo42 was built for. When the infrastructure improves, so does the opportunity for the merchants we work with.