At first glance, South Africa looks like an easy market to enter. All you need to do is switch on international card rails through your existing PSP, maybe add a gift card option, and suddenly you're "live." On paper, that looks like market coverage. It's fast, it's familiar, and it doesn't require any new infrastructure or local relationships.

But what looks clean and simple from the outside doesn't match the reality on the ground. Millions of South Africans who want to buy, subscribe or check out simply can't. It's not that they don't want to; it's that the payment options in front of them don't work for how they actually pay. And that single gap quietly drains billions in potential revenue.

The hidden limits of international card rails

For many global brands, international card rails feel like the easiest starting point. They're quick to set up, don't require additional licensing, and let merchants plug into an existing global payments stack. It's a shortcut that promises reach without the complexity of going local.

But in South Africa, that approach only scratches the surface of the market. Most consumers never make it to the end of the checkout journey because the rails they're offered weren't built for them. Credit card penetration in South Africa is relatively low compared to many developed markets. Estimates suggest that fewer than one in ten South Africans own a credit card. Surveys by the South African Reserve Bank and the World Bank put ownership between 8% and 11% of adults, depending on methodology and demographic segment.

Even within that small group, not all cards can be used for international transactions, and many banks apply extra security measures or default blocks that require consumers to manually enable international transactions. Debit cards face similar challenges. Most are not automatically enabled for international e-commerce, meaning that many customers can browse, add to their cart, and still have no way to complete the purchase.

Even when an international transaction is approved, it often comes with extra costs. South African banks typically charge between 2% and 2.75% in additional foreign transaction fees on international transactions. For someone living in a country where every rand counts, that's not a minor inconvenience. It's a real barrier. And if that's not enough friction, some banks block international transactions outright as a fraud prevention measure, forcing consumers to navigate additional steps in their banking app before they can try again.

What feels like a quick win for merchants is, in reality, a closed door for most of their potential customers. People want to pay. The problem is, they're shut out of the process. And when payments fail, trust erodes, churn creeps up, and revenue leaks away. International card rails may give the illusion of coverage, but in South Africa, they're anything but.

Why merchants default to this setup

It's easy to understand why so many global merchants default to international card rails. Expanding into a new market is complicated. Timelines are tight, resources are limited, and the pressure to show early traction is real. Integrating local payments can feel like a hurdle that can be dealt with later.

International card rails offer a tempting shortcut. It's fast, often taking just a few days to activate. It's simple, since it uses the same infrastructure already powering other markets. And it feels sufficient because card networks are seen as universal.

The problem is that what's easy to implement isn't necessarily what works best. When merchants rely on international card rails alone, they're building their entire market entry on the slimmest possible foundation. It's like launching a new product and making it available to only 10% of the population. You may technically be live, but you're not actually participating in the real market.

The cost of the blind spot

The gap between perception and reality has very real consequences for both consumers and merchants.

For consumers, the impact is immediate and personal. South African banks typically charge between 2% and 2.75% in extra international transaction fees on certain subscription payments, like streaming, gaming or software services. That might sound small, but over time, those charges quietly add up, making everyday digital services more expensive than the advertised price. And that's before counting the purchases that never happen at all because of declined payments, surprise FX spreads or blocked cards at checkout. Every extra step or unexpected cost pushes customers further away from trusting the brand they're trying to pay.

For merchants, the cost is even bigger. Relying only on international card rails means effectively limiting reach to the small minority of South Africans who have cards enabled for international transactions, and excluding everyone else at the point of checkout. It also means living with higher decline rates and unpredictable approval patterns, because international transactions are more likely to be flagged or rejected by banks. On top of that, retry logic often reflects payment cycles in the US or Europe, not local salary patterns in South Africa, which can amplify failed payments and increase churn.

This isn't just a payment infrastructure problem; it's a reach, trust and revenue problem.

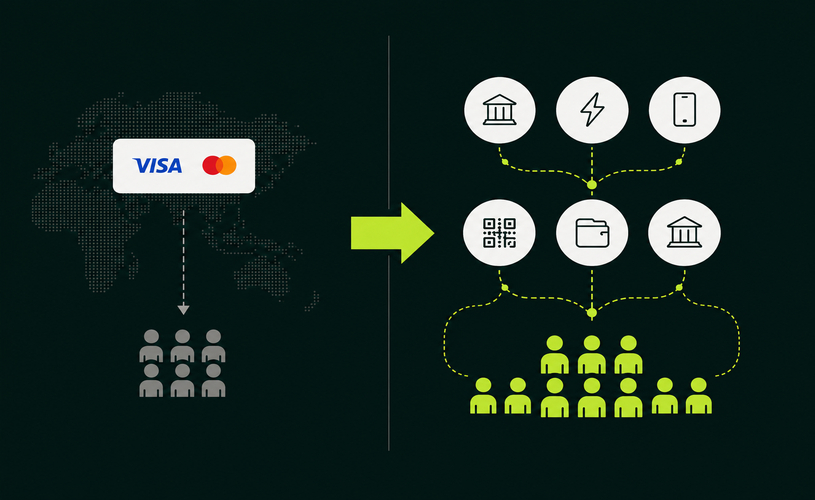

A payment landscape built on choice

Here's what many global merchants miss: South Africa isn't an immature market waiting for card penetration to grow. It's a mature, preference-driven payments ecosystem built on a diverse set of rails that reflect how people actually move their money.

Card payments account for approximately 43% of transactions, which already indicates that they're far from universal. Account-to-account or instant EFT methods account for 22 to 25%, while digital wallets sit between 15 and 20%. Layer on top of that 21 million Capitec Pay transactions and 16.7 million DebiCheck collections every month, and you get a much clearer picture.

When EBANX integrated Capitec Pay into its cross-border offering, it unlocked access to around 24 million users with conversion rates above 85%. That isn't a niche. That's the mainstream. And it proves what happens when merchants build with local payment preferences in mind instead of treating them as an afterthought.

Localisation isn't just UX, it's revenue

Too often, localisation is treated like a nice-to-have or something that can make the user experience smoother once the market proves itself. But payments aren't a cosmetic layer. They're the difference between people being able to pay and being locked out of the process entirely.

When merchants offer payment methods that align with local habits, their reach expands dramatically, connecting them to the 80% of banked adults who can't or won't pay with international transactions. Conversion rates climb because people are using methods they trust and understand. And costs fall, because they're no longer paying the extra layers of cross-border fees and FX spreads that come with international processing.

Most importantly, trust grows. Customers feel more confident paying when the experience matches how they usually transact. That confidence compounds over time, lowering churn, increasing lifetime value and building brand affinity in a way that international card rails never can.

What happens if you don't localise

The cost of inaction is real. Merchants who stick with international card rails only are choosing to leave most of the market untapped. They face limited reach, higher failure rates and abandoned carts, unpredictable revenue cycles and higher processing costs. They also face increased churn as customers lose trust after being hit with hidden fees or blocked payments.

In a trillion-rand digital economy, that's not just a missed opportunity. It's a strategic weakness. The consumers are there. The demand is there. The infrastructure is there. The checkout isn't.

Unlocking the real market with local card rails

International card rails are a starting point, not a strategy. South Africa is a mobile-first, digitally savvy market with deep local rails that already work at scale. With the right partner, merchants can bridge gaps in compliance, FX and settlement and actually reach the customers who drive growth.

That's where Novo42 comes in: we help global merchants launch quickly and compliantly without the cost or complexity of setting up local entities. We connect you to the local payment rails South Africans already use, built with intelligent retry and settlement flows that work with the market, not against it.

In South Africa, local payments aren't optional. They're how you unlock the 90% of consumers who can't pay you today.